CarLevel Insights – When we talk about car insurance, most people think the only decision is picking the cheapest option. But the truth is, the cost is only one piece of the puzzle. The real challenge is understanding what you’re actually getting—and what you’re not. That’s why coverage comparison insurance is more than a simple price check. It’s about evaluating the coverage level that protects you in real life, not just on paper.

We’ve helped many people who thought they were smart shoppers until they had to file a claim. Suddenly, they realized their policy didn’t cover what they expected. The good news is you don’t have to learn the hard way. With the right factors in mind, you can compare policies like a pro—and make a decision you won’t regret.

Why Coverage Comparison Insurance Needs a Clear Framework

When you start comparing insurance coverage, it’s easy to get overwhelmed. Insurance companies employ different words, different limits, and different language. That’s why you need a clear framework. Without it, you can mistakenly compare the wrong things, or worse, miss significant gaps.

A framework helps you see the full worth of a policy—not just its price. In this way, you can select insurance that is suitable for your requirements and level of risk, as the comparison is made objective and organized. This is especially important in auto insurance because one unexpected accident can turn into a major financial burden.

The Problem with Comparing Only Price

Choosing the cheapest insurance without verifying the specifics is the most common mistake individuals do. Although the most affordable coverage may seem appealing at first, it may not cover you enough in the event of an emergency.

We’ve seen examples when consumers paid less every month, only to learn their coverage wasn’t adequate after an accident. They were suddenly accountable for costly repairs, medical bills, and potentially legal fees. The premium may have been little, but the financial impact was significant.

That’s why coverage comparison insurance should always include a deeper look at coverage levels. Price is important, but it’s not the full picture.

Why “Coverage” Isn’t Always What It Seems

“Coverage” sounds simple, but it’s not. Two policies can look similar but behave very differently when a claim happens. Coverage levels can vary in:

- the limits they offer

- the exclusions they include

- the conditions they require

- the claims process they follow

This is why many people feel confused when their insurance doesn’t pay as expected. They assumed coverage meant protection. But in reality, coverage is a promise with conditions.

That’s why a strong coverage comparison insurance approach is to look beyond the labels and understand the real scope of protection.

The 6 Factors to Compare in Coverage Levels

Now let’s get into the heart of the matter. These are the six factors that truly matter when you compare coverage levels. If you focus on these, you’ll be able to make a smart, confident decision.

Factor 1: Liability Coverage Limits

Liability coverage is the foundation of auto insurance. It protects you if you cause an accident and injure someone or damage their property. But not all liability coverage is created equal.

The key here is the limits. A low limit may save you money upfront, but it can leave you vulnerable if the accident causes serious injury or significant damage. You all should think about worst-case scenarios, not just average situations.

When we compare liability limits, we look at:

- bodily injury limits per person

- bodily injury limits per accident

- property damage limits

A policy with higher limits may cost more, but it gives you stronger protection when it matters most.

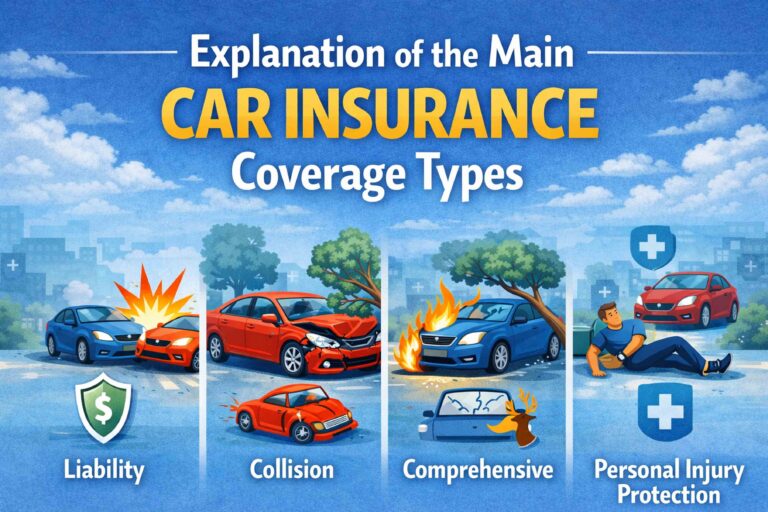

Factor 2: Collision vs Comprehensive Coverage

Collision and comprehensive are often confused, but they protect you in very different situations.

Collision coverage pays for damage to your car if you hit another vehicle or object.

Comprehensive coverage protects you from non-collision events like theft, vandalism, fire, or natural disasters.

Many people skip one of these to reduce costs. But that decision can backfire if your car is damaged in a situation you didn’t anticipate.

When comparing policies, check whether both coverages are included, what the limits are, and how they handle repairs. A policy may offer collision, but with restrictions that make it less useful.

Factor 3: Medical Payments / PIP

Medical payments and Personal Injury Protection (PIP) are coverage options that help pay medical expenses after an accident, regardless of fault. These can be especially valuable if you or your passengers get injured.

Some policies include this coverage, while others don’t. Even when included, the limits can vary widely.

We often see people underestimate medical costs. A minor injury can turn into expensive treatment, and if you don’t have the right coverage, you may end up paying out of pocket.

So when you compare coverage levels, make sure you understand the medical coverage available and whether it’s sufficient for your needs.

Factor 4: Uninsured/Underinsured Motorist Coverage

This is one of the most overlooked factors, but it can be a game changer.

Uninsured/underinsured motorist coverage protects you if you’re hit by a driver who doesn’t have enough insurance—or any insurance at all. Sadly, this happens more often than people realize.

Without this coverage, you could be left paying for repairs and medical bills that the other driver can’t cover. That’s why this factor matters in a serious way.

When comparing policies, you should check:

- whether uninsured/underinsured coverage is included

- what the limits are

- how the policy handles disputes and claims

This factor can be the difference between financial recovery and long-term loss.

Factor 5: Deductibles and Premium Balance

Deductibles are the amounts you must pay out of pocket before your insurance benefits kick in. It’s tempting to select a high deductible because it reduces the rate. However, a large deductible can become an issue if you require repairs and cannot afford the out-of-pocket expenses.

A smart comparison considers the balance between:

- monthly premium

- deductible amount

- likelihood of a claim

We recommend thinking about your financial comfort. If you can’t comfortably pay a high deductible, the lower premium isn’t worth the risk.

This factor is one of the most practical elements in coverage comparison insurance because it affects your real-world expenses.

Factor 6: Policy Exclusions and Endorsements

Exclusions are the situations your policy does NOT cover. Endorsements are optional add-ons that expand coverage.

These are often hidden in the fine print, but they can be the most important part of the policy.

For example, a policy might exclude certain types of damage, or require specific conditions to be met. Without reading exclusions, you might assume you’re covered when you’re not.

Endorsements can be very valuable, too. They allow you to customize your coverage based on your real risks.

When you compare policies, you should:

- read the exclusions carefully

- check whether endorsements are needed

- understand what is included and what is not

This is the final step to make sure you’re truly protected.

How to Use These Factors to Make a Smart Decision

Now that we’ve covered the six factors, the next step is using them in a practical way. Comparing policies isn’t just about reading terms—it’s about making a clear decision based on your personal needs.

Use a Comparison Table to See Real Differences

A simple comparison table can be incredibly powerful. Write down each factor and the corresponding details from each policy. This makes it easy to see where policies differ and where they match.

Here’s a simple example:

| Factor | Policy A | Policy B |

| Liability Limits | 100/300/50 | 50/100/25 |

| Collision | Included | Included |

| Comprehensive | Included | Not included |

| Medical/PIP | 10,000 | 5,000 |

| Uninsured Motorist | 100/300 | Not included |

| Deductible | 500 | 1,000 |

| Exclusions | Limited rental coverage | Limited rental coverage |

This kind of comparison makes the decision much clearer. You can quickly see which policy offers better protection and which one leaves gaps.

Match Coverage to Your Driving Risks (Not Just Your Budget)

Your decision should reflect your real driving risks. If you live in a busy city, your risk of accidents may be higher. If you drive long distances, you might need stronger coverage. If you have a newer car, comprehensive coverage may be more important.

We always recommend asking yourself:

- What are the real risks I face?

- What can I afford if something happens?

- What coverage will protect me financially?

Your budget matters, but your protection matters more. A smart coverage comparison insurance decision is one that balances both.

Conclusion

Choosing the appropriate Coverage Comparison Insurance is not an easy undertaking, but it does not have to be complicated. When you evaluate policies based on these six characteristics, you go from guessing to making a confident decision. Your will be able to determine the true worth of each policy and select coverage that genuinely protects you.

Remember: insurance is not just a monthly cost. It’s a safety net. And the right safety net should be strong enough to catch you when you need it most.

Frequently Asked Questions (FAQ)

What does “coverage comparison insurance” really mean?

When we mention coverage comparison insurance, we don’t simply mean the price. We mean looking at the actual protection provided by each policy—limits, exclusions, deductibles, and scenarios covered. Consider comparing two safety nets: one may appear comparable, but one may have flaws that you don’t discover until you fall.

What is coverage comparison insurance?

Coverage comparison insurance is the process of comparing insurance policies

How do I know if my liability coverage is enough?

Liability coverage is determined by your risk level and financial circumstances. We normally propose going beyond what you can afford and considering what you could lose in the worst-case scenario. If you cause a serious accident, insufficient liability limits may force you to pay out of pocket or face legal consequences. A smart rule of thumb is to create restrictions that safeguard your assets and income, rather than just your monthly budget.

Is collision coverage worth it if my car is old?

This is a common question. Collision coverage may not be economically viable for older vehicles with low values. However, we have seen cases in which an unexpected accident left someone with a total loss and no money to replace their vehicle. If your car is necessary for business or daily life, collision coverage may still be worthwhile, even if the vehicle is older.

What are endorsements and should I use them?

Endorsements are add-ons that enhance your policy. They can be very helpful if your standard policy doesn’t fully match your needs.

Can I compare policies even if I’m not sure what coverage I need?

Absolutely. In fact, the comparison process helps you understand your needs better. Start with the six factors in the checklist, then think about your driving habits, vehicle value, and financial comfort.