CarLevel Insights – When we talk about insurance, most people think it’s simply a matter of choosing the cheapest plan. But in reality, the cheapest plan is often the best plan when insurance plan comparison. The most important thing is that the coverage works with your budget, lifestyle, and actual dangers. For this reason, comparing insurance policies is more than just a chore; it’s a strategic move that may help you avoid unpleasant financial shocks.

A lot of individuals have gone with ideas that were reasonable on paper, However, they later learned that the plan did not cover what they needed. It’s not because they were careless; it’s because the differences between plans are often hidden in details. That’s why we want to help you compare insurance plans in a way that’s simple, practical, and real.

Why Insurance Plan Comparison Is More Than a Price Check

Comparing insurance policies can be daunting since each provider utilizes different phrases and systems. If you merely observe the price, you’ll just see the surface. A good comparison digs deeper into what you’re really paying for—and what you could be missing.

An insurance comparison plan functions similarly to a promise. However, not all promises are equal. Some plans offer more coverage but cost more, while others claim less and cost less. The trick is to understand your own needs. Otherwise, you risk paying for something you won’t use—or, worse, missing out on protection when you need it the most.

Why Most People Compare Plans Incorrectly

The most common mistake is comparing plans based on one or two features only, such as:

- premium cost

- coverage names

- brand reputation

But the real differences are often in the details. For example, two plans may both say “full coverage,” but one might have higher limits, better claim support, or fewer exclusions. This is why we always recommend a deeper comparison, not just a quick scan.

The Real Goal of Insurance Plan Comparison

The goal is not to find the “best” plan. The goal is to find the plan that fits you. Your driving habits, your car value, your financial comfort, and your risk tolerance all matter. If you choose a plan that doesn’t match your situation, you may feel safe—but you won’t be protected when it matters.

The Core Elements of Insurance Plan Comparison

When we insurance plan comparison, the tricky part isn’t just looking at a list of benefits. It’s knowing which parts actually matter in real life. Sometimes a plan’s fancy nomenclature or claims of “full coverage” make it seem fantastic, but the specifics reveal otherwise. We like to utilize a straightforward checklist because of this. It enables us to concentrate on the essential components that truly demonstrate what a strategy will accomplish for you, particularly during times of greatest need.

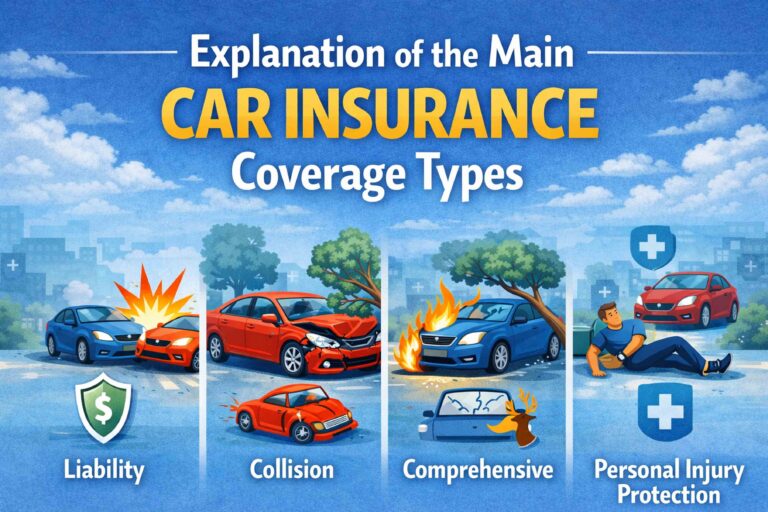

Coverage Types and Limits

First, look at what types of coverage are included:

- liability coverage

- collision coverage

- comprehensive coverage

- medical coverage

- uninsured motorist coverage

Then, check the limits. Limits determine how much the insurance will pay. A plan with low limits may look affordable, but it can be dangerous if a serious accident happens. We always recommend choosing limits that match your risk and your financial ability.

Deductibles and Premium Balance

Deductibles and premiums are the two sides of the same coin. A lower premium usually means a higher deductible, and vice versa. When comparing plans, don’t just pick the cheapest premium. Think about what you can afford to pay in a real accident.

A plan may look cheaper monthly, but if you can’t afford the deductible when a claim happens, the plan becomes a financial burden.

Claim Process and Support

This is where many people get surprised. A plan may offer good coverage, but if the claim process is slow or complicated, you may face stress and delays. We recommend checking:

- how fast claims are processed

- whether the insurer has a strong customer support system

- how easy it is to file a claim online or via app

- A good plan should not only cover you, but also support you when you need it.

Policy Exclusions and Conditions

Exclusions are the situations that the plan does NOT cover. Conditions are rules you must follow to receive coverage. These are often hidden in fine print, but they can be the most important parts of the policy. For example, some policies exclude certain types of damage to the car or require certain conditions to be met. If you don’t read the exclusions carefully, you might assume you’re covered when you’re not.

How to Compare Insurance Plans Without Getting Confused

After discussing the key components, the true question is how to compare plans without becoming confused. The secret is straightforward: don’t attempt to mentally recall anything. When you compare plans side by side, you may easily identify differences, such as coverage gaps or hidden expenses. We’ve done this ourselves, and honestly, it feels much less confusing when you write it down.

Sometimes a plan looks fine until you put it next to another one and realize, “Oh, this one has better coverage but higher deductible,” or “this one excludes the thing I care about most.” That’s why the comparison step matters. It’s not about being perfect—it’s about being clear.

Create a Simple Comparison Table

The easiest way to compare methods is to create a table. Write down the most important parts of each of your plans and compare them side by side. This can highlight differences and help you remember important details. a simple table helps you see which plan offers better coverage, which plan has better support, and which plan fits your needs.

Match the Plan to Your Real Life

The final step is to match the plan to your real life. Ask yourself:

- Do you drive daily or occasionally?

- Do you have a new car or an older one?

- Do you have enough savings to handle a high deductible?

- Do you often drive in heavy traffic or safer areas?

Your answers will guide you to the right plan. An insurance plan that fits someone else may not fit you, and that’s okay.

Conclusion

Honestly, insurance plan comparison is one of those things that people only take seriously after they get burned once. We’ve seen it happen: someone chooses a plan that appears to be good because the price is inexpensive, but then they find themselves in a scenario where the coverage is ineffective. That is why we always advise customers to look beyond the sticker price.

When you compare plans carefully, you’ll see the true differences—such as what’s truly covered, how much the limits protect you, what you’ll pay out of cash, and how simple it is to file a claim. It might feel annoying at first, but it’s worth it. Because in the end, insurance isn’t supposed to be a monthly bill you forget about—it’s supposed to protect you when things go wrong.

Frequently Asked Questions (FAQ)

1. What is insurance plan comparison?

Insurance plan comparison means evaluating different insurance plans based on coverage, limits, deductibles, and real-world protection—not just price. It’s about choosing a plan that fits your needs, not the cheapest option.

2. Why is insurance plan comparison important?

Because two plans can look similar but behave very differently when a claim happens. Comparing helps you avoid surprises and choose the plan that truly protects you.

3. Can I compare plans without knowing insurance terms?

Yes. You don’t need to be an expert. The key is to focus on the core elements like coverage types, limits, and deductibles. You can also ask the insurance company to explain unclear parts.

4. Should I choose a plan based on premium only?

No, the premium is significant, certainly, but it’s not the whole picture. A cheap premium could mean limited coverage or hefty deductibles, and that could create headaches down the road.

5. What is the most important factor in plan comparison?

It really hinges on your specific circumstances, but the coverage limits and exclusions are typically the key factors. They’re the ones that ultimately dictate what you’re actually covered for.

6. How do I know if my coverage is enough?

Consider your car value, driving habits, and financial comfort. If an accident could cause costs beyond your savings, you may need higher limits.

7. What is a deductible and why does it matter?

Your deductible is the sum you must pay before your insurance kicks in to cover the rest. This figure is significant because it directly affects your monthly premium and the amount you’ll need to spend if you’re involved in an accident.

8. What are policy exclusions?

Exclusions are situations or damages that the plan does not cover. They are usually found in the fine print and can affect your protection.

9. How do I compare claim support?

Look at the insurer’s customer reviews, claim processing speed, and whether they offer online claim filing or 24/7 support.

10. How do I choose the right plan for me?

Match the plan to your real life: your driving habits, car value, budget, and risk tolerance. Choose a plan that gives you protection and peace of mind.