CarLevel Insights – Most people don’t wake up excited to learn about Auto Insurance Explained topics. We get it. Usually, it starts because you’re buying a car, renewing a policy, or dealing with paperwork that feels more complicated than it should be. Somewhere along the way, terms like liability, deductible, and coverage limits start piling up, and suddenly you’re nodding along without really knowing what any of it means.

We’ve seen this pattern over and over. You all aren’t careless — you’re just busy. And auto insurance has a habit of explaining itself only when something goes wrong.

That’s why we put this guide together. Not to sell you a policy. Not to overwhelm you with fine print. But to give you a clear, practical understanding of how auto insurance actually works, so when you do make a decision, it’s one you won’t regret later.

What Auto Insurance Really Is

At its core, auto insurance isn’t about paperwork or monthly payments. It’s about financial protection when real-life situations don’t go as planned. Accidents happen. Cars get damaged. People make mistakes. Insurance exists to absorb financial shocks that would otherwise hit you all directly.

Many drivers think of insurance only as a legal requirement. And yes, the law does play a role. But if insurance only existed to satisfy regulations, minimum coverage would be enough for everyone. In reality, minimum requirements are just the starting line, not the finish.

If you want a deeper breakdown of how insurance is structured and why it exists in the first place, we’ve covered that in a separate guide that explains how car insurance actually works in plain language, without drowning you in legal jargon.

How Auto Insurance Works in Real Life

On paper, auto insurance looks simple: you buy a policy, pay a premium, and file a claim when something happens. In real life, it rarely feels that clean.

The process usually starts with choosing coverage, setting deductibles, and agreeing to limits you might not fully understand yet. Then comes the quiet part — months or years where nothing happens. This is where most people stop thinking about their policy altogether.

The moment that changes is when you file a claim. Suddenly, details matter. Timelines matter. Definitions matter. And this is where many drivers realize they never truly understood how the system works from start to finish.

We’ve seen many drivers only realize how complex insurance can be after something goes wrong, which is why we walk through the entire experience in detail, from buying a policy to receiving a payout, in our guide that explains the full car insurance process from start to finish.

Understanding Coverage Types Without the Confusion

Coverage types are where most confusion begins. Liability, collision, comprehensive — they all sound technical, but each one answers a very simple question: what kind of problem does this protect me from?

Liability coverage deals with damage or injuries you cause to others. Collision focuses on damage to your own vehicle after an accident. Comprehensive steps in when the damage isn’t related to a collision at all — theft, weather, vandalism, and similar events.

Where people get stuck is assuming more coverage automatically means better coverage. That’s not always true. The right combination depends on your vehicle, your finances, and how much risk you’re comfortable carrying.

Instead of memorizing definitions, it helps to understand how each type of coverage works in real situations, which is why we break things down further in a practical overview of the main car insurance coverage types

At the foundation of most policies is liability protection, and if you’ve ever wondered what it actually covers and where its limits are, we explain how liability car insurance really works in everyday terms.

There’s also a point where basic protection may no longer be enough, and knowing when full coverage starts to make more sense than liability can prevent costly surprises later on.

Deductibles, Premiums, and Why Your Price Isn’t Random

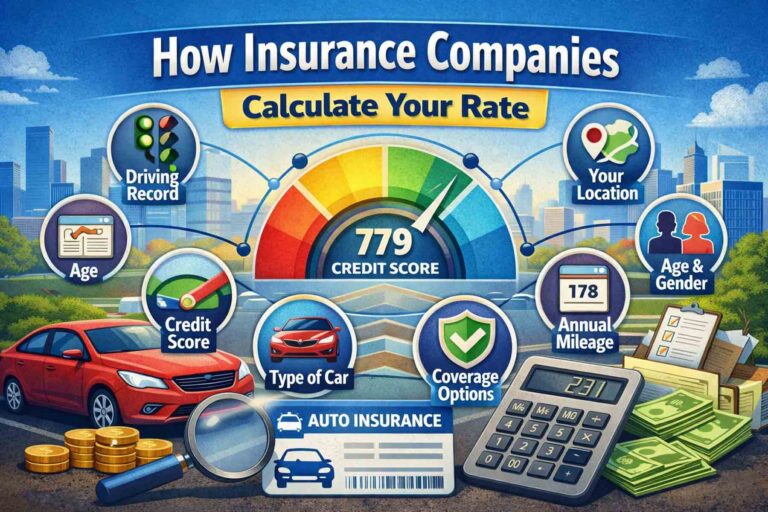

One of the biggest misconceptions we hear is that insurance prices are arbitrary. They aren’t. Every number on your policy reflects a risk calculation, even if insurers don’t always explain it clearly.

Your premium is what you pay to stay insured. Your deductible is what you agree to pay out of pocket before insurance steps in. Choosing a higher deductible usually lowers your premium, but it also means taking on more financial responsibility when something happens.

This trade-off is personal. Some drivers prefer predictable monthly costs. Others are comfortable taking on more risk upfront to save long-term. There’s no universal “right” answer — only what fits your situation.

One detail many drivers overlook is the deductible, even though it plays a major role in what you pay after an accident, which is why we explain how deductibles affect what you pay out of pocket in a separate guide.

Your monthly premium isn’t pulled out of thin air, and understanding the main factors that influence your insurance premium can help you spot pricing that actually makes sense.

Behind the scenes, insurers rely on data models and risk assessments, and we take a closer look at how insurance companies calculate individual rates so you know what’s really being evaluated.

Legal Basics Every Driver Should Understand First

Every state sets minimum insurance requirements, but those limits are designed to protect the system — not necessarily you all as individual drivers. Minimum coverage helps ensure there’s some financial responsibility after an accident, but it often falls short in real-world scenarios.

Medical costs, vehicle repairs, and legal claims can easily exceed minimum limits. When that happens, the remaining costs don’t disappear. They land on the driver who caused the accident.

Understanding what your state requires is important, but understanding what those requirements don’t cover is even more important.

While every state sets minimum standards, those numbers don’t always reflect real-world costs, so it’s important to understand what the law actually requires drivers to carry before assuming minimum coverage is enough.

Auto Insurance Isn’t One-Size-Fits-All

No two drivers have identical insurance needs. A new driver faces different risks than someone with decades of experience. A paid-off vehicle comes with different decisions than a car under financing or lease.

This is why generic advice can be misleading. Insurance decisions should reflect your driving habits, financial situation, and stage of life — not just what’s cheapest this month.

Insurance decisions also change depending on experience level, and for anyone just starting out, we’ve put together a practical guide for new drivers navigating insurance and their early coverage choices.

How to Use This Guide to Make Better Insurance Decisions

This article isn’t meant to replace detailed research. It’s meant to organize it.

We recommend starting with understanding what insurance is meant to do, then learning how coverage types work, and only after that focusing on pricing. When you reverse that order, confusion is almost guaranteed.

Use this page as your map. Then follow the links that match your situation. That’s how you move from guessing to choosing with confidence.

Conclusion

Auto insurance doesn’t have to feel like a guessing game. When you understand how policies are structured, why prices vary, and where coverage actually matters, the decisions become clearer — even if they’re not always easy.

We believe informed drivers make better choices, not because they know every term, but because they understand the trade-offs. If you all take one thing from this guide, let it be this: insurance works best when it’s chosen deliberately, not rushed through at the last minute.

Start with understanding. The right policy tends to follow.